By Jim Plaxco, President, Chicago Society for Space Studies

Based on a presentation given at the 2020 Lunar Development Conference

In considering the Moon as a future economic resource there are a number of factors that must be considered when evaluating the economic sustainability of commercial development activities on the Moon and in cislunar space.

With respect to sustainability, it is unfortunate that the term has increasingly become little more than a slogan. In the context of this article, sustainability simply means that over time there is ongoing positive economic growth in lunar-related commercial activities. Specifically, that lunar commercial ventures are profitable; that lunar economic growth in terms of GDP is greater than the associated cost of living growth; that economic diversification increases; that lunar ventures are competitive in attracting fresh capital investments; and that those living off-Earth will experience a continual improvement in their standard of living.

There are several assumptions that I make in this presentation with each having a differing degree of importance. These assumptions are that:

- market size and projected growth makes investment justifiable

- a mining dependent economy is not a bad thing

- transportation costs converge

- historical economic analogs are generally applicable

- factor overlaps are beneficially reconcilable

The first assumption, that there is a viable market for lunar products, is critical. A viable market is one for which the size of the market and the demand price points for the goods and services are such that the various businesses in the market can succeed. Further, that there is sufficient projected market growth so as to make a lunar economy increasingly practical and efficient over the longer term. Not to be overlooked is the relevance of market growth with respect to its linkage to GDP growth, which on a per capita basis is linked to a society’s standard of living.

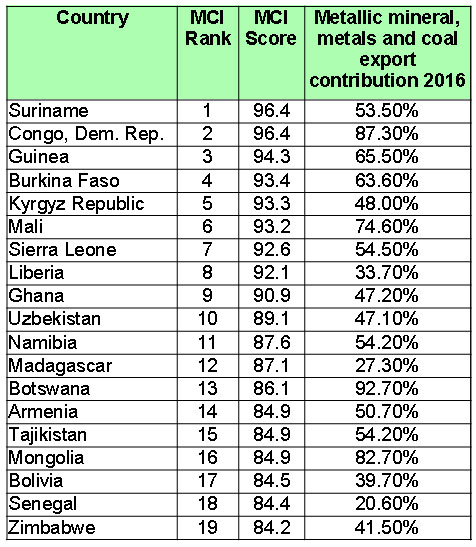

The second assumption I make is that a mining dependent economy is not a bad thing for the Moon. With respect to Earth’s nations, there is an inverse relationship between economic dependence on mining activities and overall economic development. In Mining, Minerals and Sustainable Development, Roderick Eggert states that “ mineral-dependent nations include some of the poorest and worst performing economies in the world. Mining does not always contribute to sustainable economic development.” 1 In the International Council on Mining and Metals Mining Contribution Index,2 the twenty five nations with the highest index value have per capita GDPs that are significantly below average. For reference, see Table 1.

Table 1. The role of mining in national economies mining contribution index 2018

However, space resource mining represents a unique situation to which the traditional criticisms of a mining, or resource extraction, dependent economy should not apply. This is due to there being a non-traditional political environment and a high order technological environment. These two fundamental differences make it highly unlikely that we will see the same set of scenarios that make dependence on extractive industries a bad play here on Earth.

One caveat worth considering is that significant efforts are being undertaken to increase the degree of automation in terrestrial mining operations – which means that the role of human labor in terrestrial mining is convergent with the role of human labor in lunar mining.

My third assumption is that transportation costs can converge. The demon that has forever plagued the dreams of space settlement advocates is the demon of transportation costs. In a 2007 BBC documentary, Jerry Kulcinski of the University of Wisconsin – Madison stated that “If we had gold bricks stacked up on the surface of the Moon, we couldn’t afford to bring them back… There is nothing that we know of in the solar system that is worthwhile going out to get to bring back to the Earth.” 3 At the time this statement was made, gold was selling for $10,000 per pound. For comparison, in 2017 I looked into trans-Atlantic shipping costs and discovered that I could ship a cargo of water from New York to Cairo Egypt at a list price of 18 cents a pound. It is this transportation cost differential that every space-based business will have to overcome if it is to sell goods into Earth’s various markets.

Arguably, the biggest assumption is that the product of a lunar economy can be exported into the Earth economy with a transportation cost differential that is small enough that it can be competitive given a large enough lunar production cost advantage. This can be represented by a generalized product cost function:

Lc(K,L,T,N,O,M) < Ec(K,L,T,N,O,M)

where Lc is the cost to a lunar business to deliver its product to customers in the Earth market and Ec is the cost to an Earth-based business to deliver its product to the same Earth customer. The individual cost components are categorized as capital (K), labor (L), transportation (T), natural resources (N), general overhead (O), and miscellaneous costs (M) like taxes and assorted consumables.

It must be pointed out that the requirement for a production cost advantage for lunar and cislunar products need not apply to those products for which there is not a terrestrially produced alternative. One example of such a product would be a manufactured good created using zero gee production facilities. Another example would be the export from the Moon of a high value natural resource that is more abundant locally than on the Earth – the leading example being Helium-3 – assuming of course that Helium-3 fueled fusion reactors become a reality and consequently increase the commercial value of Helium-3.

The fourth and most reasonable assumption made is that existing economic models apply equally well to non-Earth economies. For example, in terms of innovation, growth, and social well-being, communist/socialist economic systems don’t work on Earth. Therefore, there is no reason to believe that they will work in a lunar or cislunar setting.

What this means is that our existing trade models can be used in the construction of simulations of a space economy that involve operations on the Moon, on asteroids, and in free space. Specifically, the traditional trade models that we would want to consider using are the Ricardian Model which measures comparative advantage based on differences in technology; the Heckscher-Ohlin Model which measures comparative advantage based on factor and natural endowments differences, and the Specific Factors Model which measures comparative advantage based on those endowments that are immobile across industries

The final assumption being made is that factor overlaps can be beneficially resolved. Given that there will be demand overlap for use of the factors of production impacting a space economy’s total output, I am assuming that not only is usage allocation of the various factors reconcilable but that the competing demands will be reconciled in a manner that has a positive, rather than negative, impact on total economic activity. There is a finite supply of labor, capital, natural resources, energy, land, etc. The challenge is for the competitive system to allocate these factors across industries in such a way that total system output, or value, is maximized.

The Mars Society recently held a Mars City State Design Competition and I was a member of a team that entered the competition. At times I was dismayed by some of the policy desires on the part of some members of the economics team since I saw those policies as being detrimental to economic success. For example, the push for the use of short-term, non-transferable property leases rather than the use of property deeds that allowed for direct ownership transfer to another party. What this meant was that, for example, a business would not own the property it built its factory on and at the end of the lease period the landlord, in this case the State, would retake control of the property and could then lease that property, along with the factory, to another entity. Is there any business anywhere that would agree to such terms? Lack of clear and well defined property rights would be severly detrimental to the private and commercial development of the Moon.

With respect to the competition’s guidelines, I want to call attention to the premise put forward by the Mars Society. The contest definition states that “The city state should be self-supporting to the maximum extent possible – i.e. relying on a minimum mass of imports from Earth… imports will always be necessary, so teams will need to think of useful exports – of either material or intellectual products that the colony could produce and transport or transit back to Earth to pay for them.” 4 This statement implies that Earth will be the only market for Martian exports and that the Martian economy has to be as self-sufficient as possible.

Consider what a high degree of self-sufficiency means. With economic globalization we have a system of trade that integrates the world’s economies and leverages the system of comparative advantages, enhances the value of mass markets, and consequently results in greater total economic output, which on a global basis raises the overall standard of living.

The system called for in the Mars competition, which represents an all too commonly held view of space activists, is an autarkic system that will result in a lower standard of living for all concerned. That the only expected trading partner for Mars is defined as being the Earth suggests a mercantilistic relationship. By mercantilism, I mean a form of economic governance that treats non-terrestrial centers of activity as being subsidiary to the parent nation or nations of Earth. However, if the goal is to create fully automated space economies where there is essentially no local human population, and the primary objective is to enrich the host nation or nations on Earth, then a mercantilistic approach does make sense.

Assuming that there are a million people living on Mars, as the Mars design competition design calls for, then it is entirely logical to expect that there will be significant human populations living on the Moon and elsewhere in the Solar System. With this in mind, trade between Mars and other non-Earth population centers will be crucial to the survival of not just the Martian economy, but the other space-based economies as well. Consider it to be the globalization of the solar system.

The desire for every off-Earth population center to be self-sufficient is understandable but when someone makes that statement, we have to ask the question of why and understand the associated costs. If autarky is considered a bad economic solution here on Earth, why would it be a good solution for someone living on the Moon? It is well established that autarky both raises the cost of living and lowers the standard of living. Autarky ignores the considerable value of a network of comparative advantages and the economic gains that trade makes possible.

Consider this thought: if a lunar colony insists on being self-sufficient when it comes to water, metals, and other goods and services, what does that mean for non-lunar asteroid mining businesses whose life blood is the market demand for water, metals, and other raw materials? If a lunar colony insists on being self-sufficient when it comes to manufactured items, what does that mean for non-lunar space-based manufacturing businesses?

Systemically, will humanity be stronger with a series of economically isolated islands or will it be stronger with a network of economically integrated nexuses?

Perhaps the most complex challenge, and the one which may have the greatest impact on the establishment of a significant private commercial presence in space, will be the governance challenge. Governance refers to all the processes of governing undertaken by some acknowledged authority that exercises control over some defined territory or set of organizations through the use of laws or some other form of power. For example, various international organizations will make loans to nations based on that nation’s adherence to principles of good governance. It is governance that defines the legal environment within which our system will operate. How an economy is regulated and governed is the single most critical determinant of whether or not that economy will be successful.

Elements of governance that are relevant to lunar commercial activities include:

- Real property rights recognition, administration, and claims resolution

- Extent to which natural monopolies are defined as being preferable to competition

- Openness to foreign direct investment

- Definition and management of transaction costs between entities

- Extent and transparency of the regulatory environment

- Definition and transparency of the liability environment

- Internally and externally defined trade barriers (tariffs, quotas, duties)

- Cost and administrative management of system infrastructure

- Administration of contract law

- Selection of a legal administrative system (common law vs civil Law)

- Definition and stability of a system of currency

Property rights for private and commercial lunar development

One governance issue that has received considerable attention is that of property rights. Current law does not provide the degree of legal clarity necessary with respect to the granting of property ownership rights to private actors. There is also the question of how property rights will be administered and adjudicated.

Peruvian economist Hernando de Soto coined the term “dead capital” to describe an asset that can not be easily bought, sold, valued or used for collateral. In short the asset, in this case real estate, is not a fungible asset. This acts as a brake on economic growth and de Soto cites it as an important factor with respect to the high level of poverty experienced by a number of nations. In writing on the issue of property and capital, de Soto clarifies the challenge: “Why have the rich nations of the world, so quick with their economic advice, not explained how indispensable formal property is to capital formation? The answer is that the process within the formal property system that breaks down assets into capital is extremely difficult to visualize. It is hidden in thousands of pieces of legislation, statutes, regulations, and institutions that govern the system.”5

Loup Brefort of the World Bank put it more succinctly when he wrote that “Experts have found out a direct correlation between a nation’s wealth and having an adequate property rights system. This is because real estate is a form of capital and capital raises economic productivity and thus creates wealth.” 6

Assuming that private property rights are acknowledged as being a necessary condition, the question then becomes one of definition, administration and pricing. And there are wrinkles that must be considered. For example, can a single entity lay claim to an entire asteroid by virtue of being the first one there? The answer may be no. But what if that entity adds value to that asteroid by despinning it or altering its orbit? What then?

And will property rights be transferable? How likely would it be that a business would build a factory on land they purchased but couldn’t sell? When it comes to property rights, three key aspects to consider are clear and secure ownership of property; clear and secure title to said property; and a clear, secure, and efficient means of transferring that property ownership to others of the seller’s choosing.

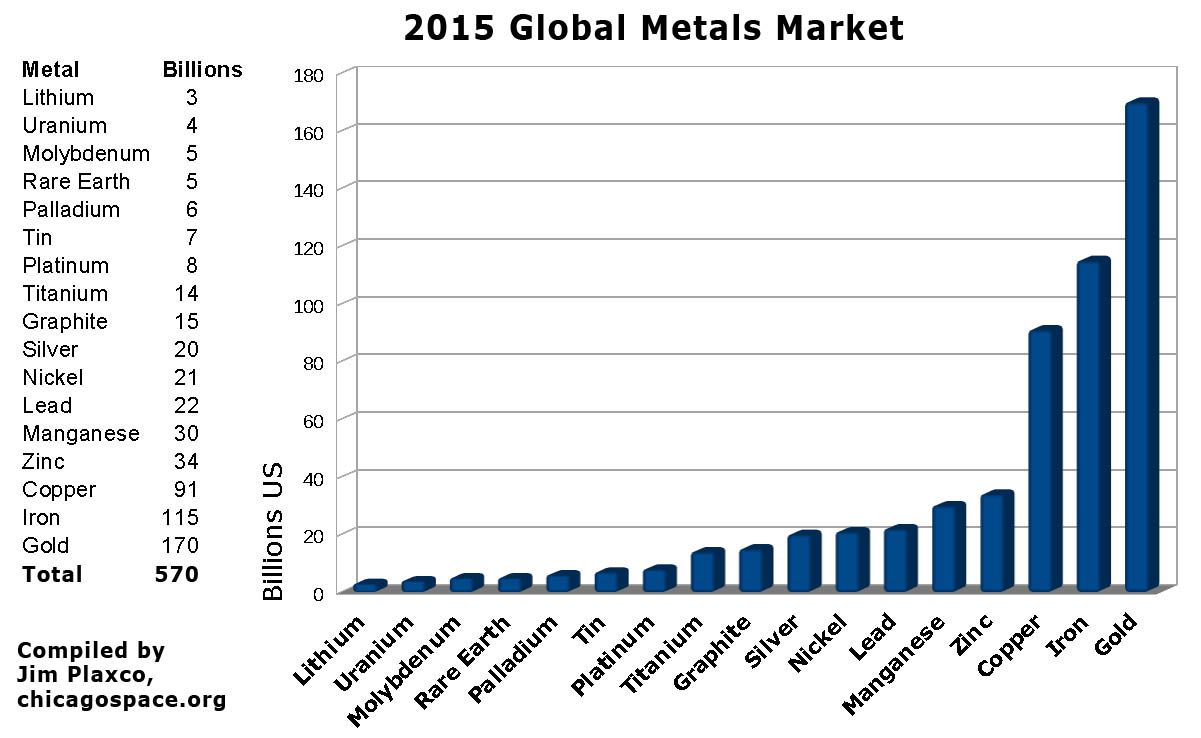

Assuming that governance issues are favorably resolved, another key issue will be that of market size and stability. For illustration purposes, I will focus on the nature and size of the market for metals. With respect to lunar and asteroid mining we have to consider the size and dollar value of the global market in terms of demand for each of the possible natural resources while paying particular attention to the Earth’s demand and the distribution of that demand across different metals.

The global metals market in 2015

According to Statista, the total global metals market in 2015 was about $660 billion7 – which is just a tiny fraction of the size of the global oil market. The distribution of the value of that demand is broken down as follows:

- Gold: $170 billion

- Iron: $115 billion

- Copper: $91 billion

- Aluminum: $90 billion

- Zinc: $34 billion

- Manganese: $30 billion

- Nickel: $21 billion

- Silver: $20 billion

- Other metals: $67 billion8

The “Other metals” category includes platinum, palladium, titanium, tin, molybdenum, uranium, and others. Smaller metals markets, like bismuth, antimony, and rhodium, were omitted from the market calculation, whose size was determined by multiplying the demand for the year 2015 by the available market prices for each metal.8

Lunar mining operations will be in competition with asteroid mining operations who will be in competition with Earth mining operations and each of these will be competing with terrestrial metal recycling operations. For example, in 2015, just over 20% of the global demand for platinum was met by recycling operations. In 2017, the fraction of platinum demand met by recycling operations had risen to 25%. 9

The question that any business entering the space metal mining market must ask is how well does the scale of space mining operations necessary to cover ongoing operating costs align with the total market size in terms of both the quantity demanded and the market price for each metal? In addition, that business needs to determine if it can be cost competitive with the market’s other producers.

An analogous situation is that of proposals for systems of solar power satellites. With respect to these SPS proposals, projected construction and operational costs have been such that the price that would have to be charged for the electricity generated would not be competitive. That means that in a free marketplace, no one would purchase SPS-generated electricity.

While we hear statements about the street value of the metals in an asteroid, what we do not hear addressed is the issue of just how much of that metal supply can be absorbed by the market, both terrestrial and space-based, over any given period of time. There is also the question of whether or not those metals can be delivered to market at a cost that is lower than the cost of their Earth-based counterparts. Lastly there is the question of how flexible space mining operations will be with respect to dealing with market fluctuations.

Linked to the size of any given market is the question of the availability of substitute goods and competing suppliers. A question to be asked is what happens to your business if your customers find an alternative supplier for your dominant good? Something to be considered is factor price equalization (FPE). The theory of factor price equalization states that the price of identical factors of production will be equalized across nations due to the international commodities trade. The market for oil is one example of this equalization or price convergence. The question to be asked is what happens to those operations whose cost of production is greater than the convergent price? An example of a commodity impacted by price convergence is oil, specifically fracking for shale oil in competition with other oil extraction operations. The experience of North Dakota serves as an excellent example of a high cost supplier attempting to survive in a low price environment.

In consideration of asteroid mining versus lunar mining, there is a large degree of overlap in the natural resources that will be mined by both operations. With respect to volatiles, there is potential overlap with the mining of carbon, hydrogen, and oxygen. With respect to metals, there is potential overlap with the mining of copper, iron, nickel, iridium, osmium, palladium, platinum, rhodium, and ruthenium. With multiple system sources of raw materials and a competitive marketplace, who will survive?

Another consideration for a lunar economy is how diversified it will be. Economies produce a broad mix of goods for consumption and/or export. A good is considered tradable based on its shelf-life and transportation costs relative to its market price. Having a larger range of tradable goods is an economic plus. Economic diversity reduces a society’s risk exposure to an economic downturn or a good’s substitution situation. An economy that produces only a limited variety of goods, as measured by an economic diversification index, is more vulnerable than an economy that is well diversified. An economic diversification index (EDI) is a measure of the number of goods a system produces and their relative value compared to the total value of all goods produced by that economic system. The lower the index value, the less diversified an economy is. An example of dependence is that of the Detroit area on the automotive industry. The automotive industry played a significant role in the economy of Detroit and the surrounding area.10As that industry’s fortunes declined so too did Detroit’s fortunes, with the subsequent drop in tax revenues exposing inherent weaknesses in the system.

An alternative to an economic diversification index is the Harvard Economic Complexity Index (ECI) which rates countries based on how diversified and complex their export basket is. The Harvard Atlas of Economic Complexity maintains their Economic Complexity Index for every country for which sufficient data is available.11 A comparison of the most economically complex nations versus the least economically complex nations is revealing. The index reveals a strong correlation between economic complexity and both per capita GDP and the United Nations Human Development Index (HDI).

Another issue for lunar industries will be that of capital intensity. I recently saw a cartoon that featured a pair of robots standing by the office water cooler in what was an otherwise empty office with one robot saying to the other “they call it the flu season.” It’s a given that it will take significant capital to build the infrastructure needed to keep people alive and well in space and on the Moon. The large scale diversion of capital from industrial construction to human habitat and life support construction means that the value that our lunarians will need to add to the lunar economy will have to be greater than the value of the output that the same capital could have produced if it had been used towards the construction of automated industrial operations.

A measure of the role of capital versus other factors, primarily labor, in generating output is capital intensity – which is the ratio of the total value of capital to total output. One way of analyzing the situation is by doing a Net Present Value analysis on the return from fully automated operations versus the return from using differing degrees of human labor in the production process.

If we were to perform a robot vs human comparison with respect to the various factors that dictate the cost of labor in a space environment, robots and automation would win in every category. It is worth pointing out that if people were operationally as cheap as robots, then we’d be sending astronauts and not robots to explore the Moon, the asteroids, and Mars.

When you consider the nature of the environment and the work and the cost profile of a robotic worker versus a human worker, robots are the clear winner when it comes to minimizing the costs of off-world industrial operations and maximizing output.

Whether or not this is desirable depends on one’s perspective on space development and space settlement. If the objective is to produce goods for terrestrial consumption, then automation should be maximized. But if the objective is to create new homes for humanity, then an approach that seeks a balance between automation and support for a human population must be pursued.

An examination of Earth’s advanced economies reveals that productivity growth and a rising standard of living are tied to an increasing reliance on capital. A business requires capital to purchase the next generation of equipment that allows it to more efficiently use the other input factors to create output. A term used to describe this increased reliance on capital is capital deepening. Capital deepening is the state where the amount of capital per worker is increasing in the economy. This is also referred to as an increase in the capital intensity. Capital deepening is often measured by the rate of change in capital stock per labor hour.

An associated measure is the capital output ratio (COR) which is the ratio of units of additional capital required to produce an additional unit of output. One example of capital deepening where we are increasing the COR is with the assembly of solar power satellites. The projected cost of construction of the 1979 SPS Design Reference was dominated by the labor costs. However, by employing automation to replace the human labor force, it has been estimated that the system cost could be reduced by a factor of 20. This increased reliance on capital is an example of capital deepening in that it uses capital to replace labor as a factor of production.

Capital deepening is a key to productivity growth which in turn drives economic growth which drives improvements in our standard of living. Productivity growth equates to a lowering of unit production costs over time. Alternatively, this can be thought of as producing the same quantity of output while using smaller quantities of inputs. The best measure of productivity is multi-factor productivity. Quoting from the U.S. Bureau of Labor Statistics, “Multifactor productivity (MFP), also known as total factor productivity (TFP), is a measure of economic performance that compares the amount of goods and services produced (output) to the amount of combined inputs used to produce those goods and services. Inputs can include labor, capital, energy, materials, and purchased services.” 12

It should be clear that capital is a key to economic growth. A study by KPMG Economics found that “growth in net fixed capital accounted for about 69% of Australia’s GVA (Gross Value Added) growth… the average annual contribution of labor to GVA growth was 18%… Multifactor productivity accounted for the residual growth in GVA, making a contribution of 12%.” 13

It’s a given that to build a business or an industry, you need capital. Private sector capital is in limited supply and it will preferentially flow to those investments that minimize risk and maximize payoff. In this context, the question is whether or not lunar industries will have what it takes to attract the investment capital they will need to build and maintain their industries.

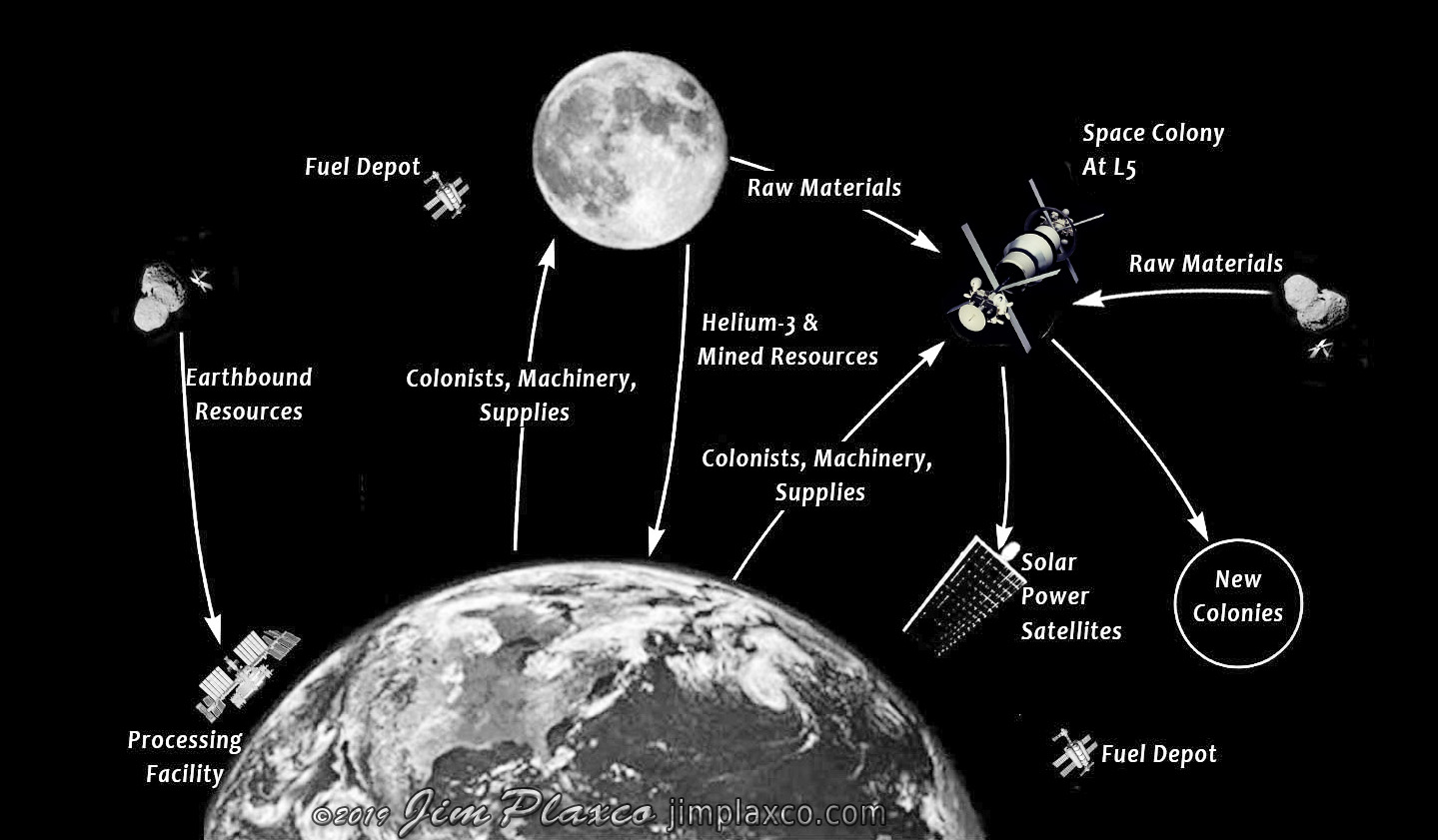

Figure 2. An example of an Earth-centric cislunar economic system.

The diagram in Figure 2 is an example of the sort of space-based economic system that space advocates have long speculated on and written about. It is a system that offers a degree of plausibility. The challenge is less with the technology and more with whether or not such a system is economically realistic. What we have is a complex equation for which there are not only unknown values for known parameters, but potentially unknown parameters that have to be considered from a modeling perspective.

In consideration of the previously referenced trade models used to analyze trade, there are four basic questions we need to ask in evaluating the plausibility of trade between Earth and non-Earth economic centers:

- What advantages will space-based industries have over Earth-bound industries?

- Are those advantages conducive to the creation of a system of mining industries?

- Are those advantages conducive to the creation of a system of manufacturing industries?

- Will those industries be able to generate sufficient value to justify the associated resource allocations and capital investments necessary to sustain them?

Regardless of which of the trade model you choose, lunar industries will be competing with both Earth-based industries and other space-based industries for markets and market share, not to mention competing for the capital required to develop infrastructure and fund the various business ventures. Whether or not such ventures will succeed or fail remains to be seen.

References

1. Roderick Eggert, “Mining and Economic Sustainability: National Economies and Local Communities,” Mining, Minerals and Sustainable Development, Oct 2001.

2. “Mining Contribution Index,” International Council on Mining and Metals, https://www.icmm.com/en-gb/society-and-the-economy/role-of-mining-in-national-economies/mining-contribution-index.

3. Mining The Moon for Helium-3, Aired 2007, BBC Documentary.

4. “Mars City State Design Competition Announced,” The Mars Society, https://www.marssociety.org/news/2020/02/11/mars-city-state-design-competition-announced/.

5. Hernando de Soto, “The Mystery of Capital,” Finance and Development, A quarterly magazine of the International Monetary Fund, March 2001, Volume 38, Number 1.

6. Loup Brefort, “Unlocking the Dead Capital”, The World Bank, November 18, 2010, https://www.worldbank.org/en/news/opinion/2010/11/18/Unlocking-the-Dead-Capital

7. “Statista Market size of selected metals worldwide as of August 2015,” Statista, https://www.statista.com/statistics/655194/commodity-metals-global-market-size/.

8. “Statista market size of selected metals worldwide as of August 2015,” Statista, https://www.statista.com/statistics/655194/commodity-metals-global-market-size/.

9. “Summary of Platinum Supply and Demand in 2017,” PGM Market Report, Feb. 2018.

10. S. F. Rushen, “Fluctuations and Downturns in a ‘Company Town’,” Growth and Change, 26 (1995).

11. “2018 Country Complexity Rankings,” Harvard Atlas of Economic Complexity, 2018, https://atlas.cid.harvard.edu/rankings/.

12. “Multifactor Productivity,” U.S. Bureau Of Labor Statistics, https://www.bls.gov/mfp/home.htm.

13. “The role of capital and labour in driving economic growth in Australia,” KPMG Research Paper, 2016.

The future market value of Helium-3, based on total reliance on Lunar resource availability and sufficient money and research invested in attaining sustained nuclear fusion, will be at a level making automated or semi-automated Lunar Helium-3 mining and refining facilities economically viable. This, of course depends on demonstrated sustained nuclear fusion in a reactor, whether the reaction is Helium-3/Deuterium or some other type of fusion reaction.